Let me show you the evidence.

HDB resale prices from 1994 to 2013

The year 1996 was the prelude to the Asian financial crisis. I'll skip all the nitty gritty of what exactly happened. If you're interested, you can search for Asian financial crisis and find out more about it. Briefly, it began with the Thai baht currency collapsing and the negative effect spread to the rest of the Asian countries.

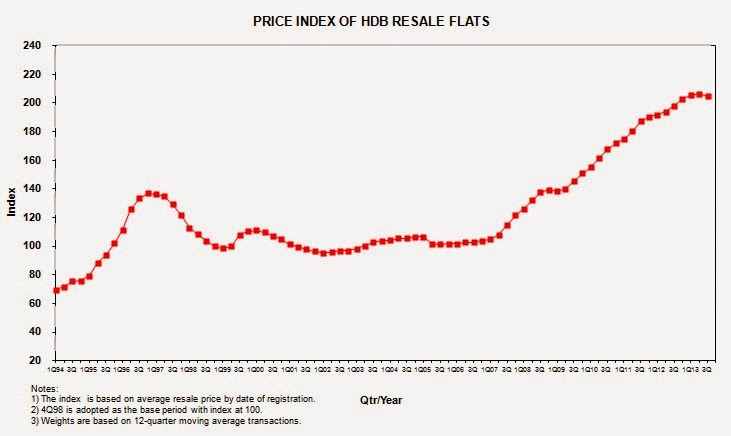

It'll be hard to remember how much HDB prices cost exactly during that time so I'll be using an indicator called HDB resale price index(RSI). This index tracks the average HDB resale prices in Singapore for each Quarter. The RSI was at a high of 136 in 1997 before it crashed to 95 in 1998. After that prices remain stagnant in the 95-110 range for 10 years until 2008.

It's hard to imagine the trend so here's a chart from HDB themselves to show the RSI trend:

As you can see, prices of HDB were up steeply before the crash. In percentage terms, RSI increased almost 100% from 1994 to 1997 before crashing 30% in 1998.

What caused the crash?

Interest rates. I'm referring to home loan interest rates. When interest rates are cheap, people take loan to buy property and when interest rates are expensive, people put on hold their buying of homes. This is one of the factors but there are many other factors too such as available number of properties, number of buyers, government policy for loans and the property market.

Will prices fall again?

Recently, the news on property market have changed. No longer does the news keep saying that property prices are hitting record high. We hearing things like number of housing sales decline, cooling measures slows down rising prices. Analyst are predicting that property prices may fall around the 5% range next year. Will prices fall again? It does seem like it will at least decline marginally or stay stagnant since there's a huge number of supply now and more coming, government has imposed many cooling measures, and interest rates are set to rise soon as US begins tapering.

What does it mean for young couples planning to get their first home now?

If you're getting married and planning to buy a new house, take into consideration that prices may fall. By how much, no one will know exactly.

Here's how you can decrease the impact that may affect you:

1) Take the HDB housing loan.

It's higher than the housing loan offered by banks now but at least it'll save you the worry of rising interest rates. Interest rates on bank loans are definitely lower now but banks will only offer fix rate for a limited amount of time. The longest i've seen is the POSB home loan which fix the rate for 4 years. HDB housing loan is not a fixed rate but it's pegged to 0.1% above the CPF OA interest rates which rarely changes. You don't want to take a bank home loan at 1% now to see it rise to 4% in the future.

2) Buy a house that you can afford comfortably.

Everyone wants to buy a big house. But who thinks of whether you can service the loan for 30 years? Avoid stretching yourself by taking too much debt. You don't want to end up having the difficulty to pay for your house forcing you to sell it prematurely. And if just nice its during the property crash that you are forced to sell, you'll sell it at a loss for sure. Remember if the property market does crash, it'll mean that the economy is not that good and it also means you're very likely to lose your job.

3) Always have an emergency fund ready

No matter what, it is important to put aside some savings for rainy days. In case you lose your high paying job, you still can survive for at least a few more months.

Retrenchment? It'll never happen to me since i'm still young. Don't say it too early. You will never know if it will happen to you. Read: Recession Heroes Ep 4 - Got retrenched at a young age of 23 but still full of passion in life

Conclusion

In conclusion, don't forget that property prices can fall. When it falls, it can stay down for 10 years or more. It has happened before and it can happen again. It may be worse or it may not be worse. Whatever it is, stay safe and don't get caught in it.

This post was sparked off by a conversation with my colleague that his sister just sold her house for a small 30k profit recently. They bought their house at the peak of 1997. That's only 30k profit after 16 years. They had to wait more than 14 years just to breakeven!

Like my articles?

You can Subscribe to SG Young Investment by Email

or follow me on my Facebook page

Related Posts:

1. The dangers of over leveraging on debt

2. How rising interest rate affects the housing loan you pay? [Guest Contribution]

.jpg)

.JPG)

.jpg)